A second glance at

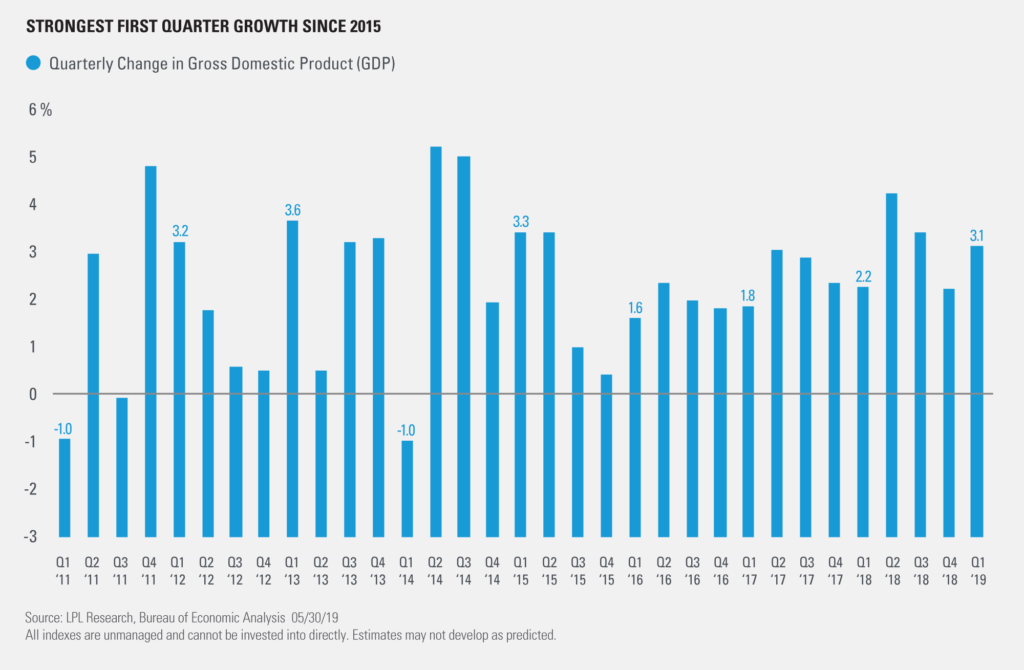

A shown in the LPL Chart of the Day, GDP rose 3.1% in the first quarter, according to the first revision released May 29. Although headline growth was revised down, it was still the biggest first-quarter GDP gain since 2015, showing the U.S. economy remained resilient against trade and political headwinds.

“We don’t think we’re heading for a recession in the near term, even after the latest trade escalation,” said LPL Research Chief Investment Strategist John Lynch. “Growth may slow as the expansion matures, but the U.S. economy has shown that it is durable enough to weather geopolitical storms.”

The drivers of last quarter’s growth were less impressive than the overall gain. Inventories and net exports still accounted for about half of first-quarter GDP growth, a temporary boost that could reverse in future quarters. Consumer spending’s contribution was revised slightly upwards, and business spending’s contribution was cut. Excluding inventories and trade impacts, GDP increased 1.5% in the quarter, its weakest “real final sales” growth since the end of 2015.

History leads us to believe that second-quarter growth could benefit from economic seasonality. The first quarter has typically been the weakest of all four quarters in this expansion, while the second quarter has been the strongest. Economic data also rebounded in April, encouraging is that business and consumer spending could fuel growth, even as the lift from net exports and inventories likely disappears. Trade is the primary risk to near-term growth, though, and it’s difficult to gauge how renewed trade tensions will impact second quarter GDP.

Overall, we expect economic growth to moderate from last quarter but still power through at a respectable pace for the 10th year of the soon-to-be longest ever economic cycle. In a worst-case trade scenario, we anticipate GDP growth of about 2% this year, in line with the average pace of growth so far in this expansion.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. The economic forecasts set forth in this material may not develop as predicted.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. All performance referenced is historical and is no guarantee of future results.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

The investment products sold through LPL Financial are not insured deposits and are not FDIC/NCUA insured. These products are not Bank/Credit Union obligations and are not endorsed, recommended or guaranteed by any Bank/Credit Union or any government agency. The value of the investment may fluctuate, the return on the investment is not guaranteed, and loss of principal is possible.

For Public Use | Tracking # 1-858738 (Exp. 05/20)