Job growth rebounded strongly in March, allaying concerns that a February slowdown was signaling the possibility of extended economic weakness.

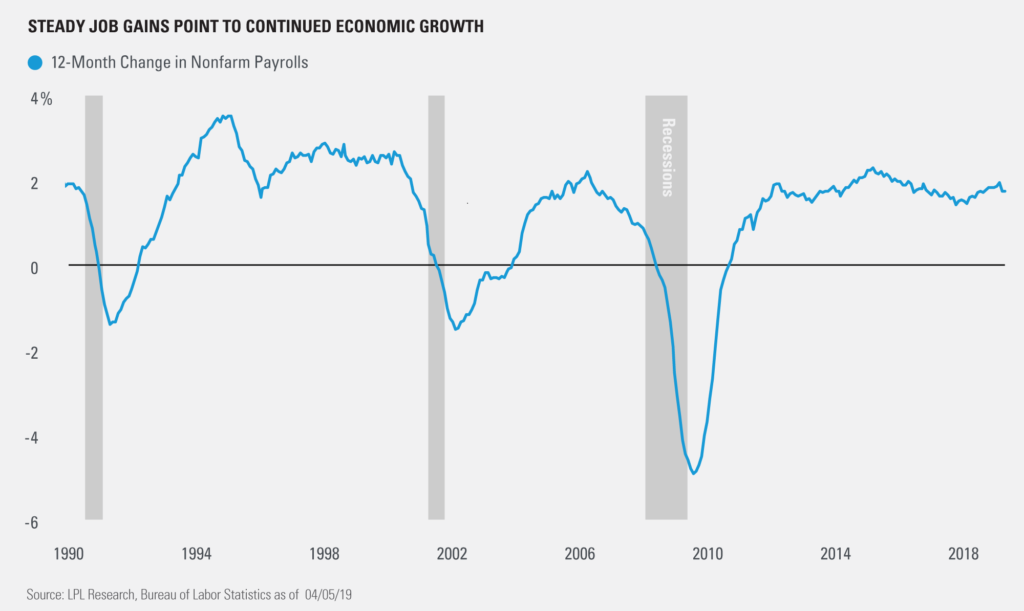

Nonfarm payrolls rose 196,000 in March, beating consensus estimates of 177,000. As shown in the LPL Chart of the Day, average yearly gains have remained largely steady. Overall the labor market remains robust for this point in the cycle, with no apparent sign of the rapid slowing that has often occurred before the onset of a recession.

“Today’s numbers confirm that February labor weakness was temporary,” said LPL Research Chief Investment Strategist John Lynch. “Labor market strength remains a bright spot in the U.S. economy, and wages are growing at a healthy pace.”

Average hourly earnings grew 3.2% year over year, slowing modestly but remaining at a level that should continue to bolster consumer confidence and support consumer spending. Wages have been one of the most telling job-market indicators to us, as year-over-year average hourly earnings growth historically has reached 4% before it threatened economic output due to added inflationary pressure. The current rate of growth should give the Federal Reserve (Fed) plenty of leeway to continue to take a wait-and-see approach on interest rates.

The unemployment rate held steady at 3.8%, near a cycle low. The labor force participation rate dipped slightly to 63

Initial jobless claims fell to a 49-year low through last week, showing that unemployment continues to decline amid solid hiring conditions. While most labor-market data serve as lagging indicators of U.S. economic health, jobless claims as a leading indicator. Historically, a 75-100K increase in claims over a 26-week period has been associated with a recession.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. The economic forecasts set forth in this material may not develop as predicted.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. All performance referenced is historical and is no guarantee of future results.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

The investment products sold through LPL Financial are not insured deposits and are not FDIC/NCUA insured. These products are not Bank/Credit Union obligations and are not endorsed, recommended or guaranteed by any Bank/Credit Union or any government agency. The value of the investment may fluctuate, the return on the investment is not guaranteed, and loss of principal is possible.

For Public Use | Tracking # 1-839992 (Exp. 04/20)