U.S. bond bulls are winning in the global search for yield.

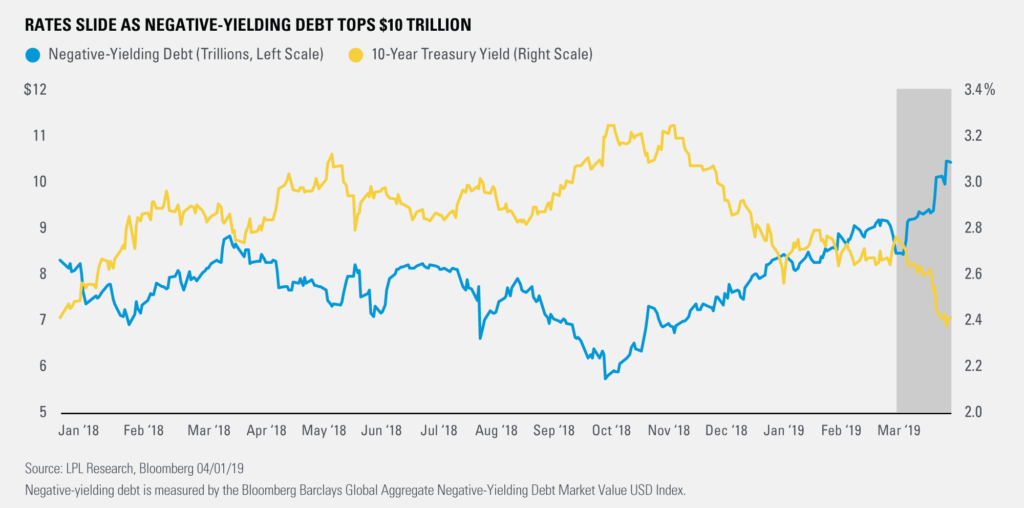

As shown in the LPL Chart of the Day, negative-yielding debt around the world has grown to $10.4 trillion, its highest point since September 2016. At the same time, the 10-year Treasury yield fell 31 basis points (0.31%) in March as prices jumped, and the Bloomberg Barclays Aggregate Bond Index notched its best monthly performance in four years.

Recent strength in fixed income has been interesting, especially amid the S&P 500 Index’s best first quarter in over 20 years. Typically, equities and bond prices move opposite one another. However, that relationship has broken down this year as global rates have felt the sting of a worldwide growth slowdown. Yields on sovereign debt for developed nations have dropped 20 to 30 basis points (0.20-0.30%) year to date, and investors in Germany’s debt are contending with negative

“U.S. debt is attractive for global investors looking for both yield and safety,” said LPL Research Chief Investment Strategist John Lynch. “We expect slightly higher inflation and continued steady U.S. economic growth, but strong global demand has capped yield appreciation.”

While the U.S. debt binge has lifted bond bulls’ portfolios, it has indirectly fueled investors’ worries about impending economic weakness and slowing inflation. Insatiable global demand for U.S. Treasuries has weighed on long-term rates, skewing economic signals from the bond market. At the end of last month, the spread between the 10-year and 3-month Treasury yields turned negative for the first time since 2007, sparking concerns that bonds could be hinting towards an impending recession. Most economic indicators we follow contradict this message, and we see low odds of a recession in the next year.

Overall, we believe that foreign demand has led to an overreaction in U.S. bond markets, to the benefit of some investors and the detriment of others. While we think global demand for U.S. debt will be higher this year, we expect recent buying pressure to ease if trade risk subsides and global data improve.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. The economic forecasts set forth in this material may not develop as predicted.

All indexes are unmanaged and cannot be invested into directly. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. All performance referenced is historical and is no guarantee of future results.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

U.S. Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. They are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

The investment products sold through LPL Financial are not insured deposits and are not FDIC/NCUA insured. These products are not Bank/Credit Union obligations and are not endorsed, recommended or guaranteed by any Bank/Credit Union or any government agency. The value of the investment may fluctuate, the return on the investment is not guaranteed, and loss of principal is possible.

For Public Use | Tracking # 1-838562 (Exp. 04/20)